In-Depth Analysis of the Security of Supply Monitor: Without Additional Policy, There Is No Business Case for Batteries

TenneT’s 2026 Supply Security Monitor confirms that batteries play an important role in preventing future electricity shortages. At the same time, the report shows that the business case for large-scale battery storage remains uncertain as we look toward 2030. This underscores the need for additional policy measures, including a fair capacity mechanism, broad availability of the TDTR, and targeted support for long-duration energy storage.

Electrification of Energy Consumption

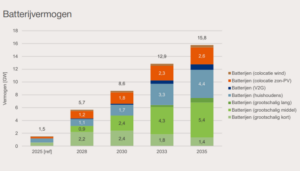

The energy transition calls for changes in energy consumption and production, including through electrification and renewable generation. TenneT forecasts growth in renewable generation from 41.1 GW today to 80.3 GW in 2035. However, the weather is unpredictable, resulting in a more volatile generation pattern compared to fossil fuel sources. During the transition to a CO2-free energy system, this could lead to temporary periods when there is insufficient electricity supply. To address this, alternatives to fossil-fuel-based regulating capacity—such as storage and demand response—are needed more urgently. TenneT therefore anticipates strong growth in battery capacity toward 2035, reaching 15.8 GW (see Figure 1).

Figure 1. TenneT’s Forecast for Battery Capacity Growth, 2025–2035

The Growing Role of Storage

TenneT anticipates growth in large-scale 2-hour batteries leading up to 2030. After that, these batteries will be partially replaced by 4-hour batteries at the same location. They do not expect to see significant growth in 8-hour batteries until 2033. Co-location with solar—and, to a lesser extent, wind—will also play an increasingly important role. Furthermore, they anticipate strong growth in home batteries due to the phasing out of the net metering program and the introduction of new dynamic rates.

ESNL welcomes the central role that TenneT says storage will play in a future energy system. We agree that at least 15.8 GW of battery capacity will be needed by 2035. This is expected to be an overly conservative estimate, as it does not account for behind-the-meter storage at businesses, for example. Batteries can help alleviate grid congestion, but according to TenneT, the relative impact per GW of batteries on security of supply will only increase ‘when storage volumes rise significantly.’ Furthermore, TenneT states that Long Duration Energy Storage (LDES) is a good alternative to fossil fuel power plants. However, the report does not sufficiently account for 8-hour batteries and forms of hydrogen and thermal storage in its analysis.

Business Case for Storage

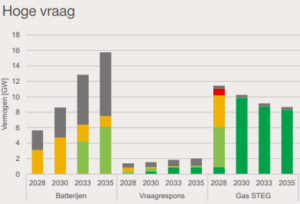

According to the Monitor, the future of flexibility is shrouded in uncertainty because it depends on the pace of technological developments, market adaptability, and the political implementation of regulations and subsidies. The Monitor therefore suggests that a large portion of battery capacity through 2030 is only ‘potentially’ viable (see Figure 2). This is despite projections of a 15.8 GW rollout by 2035. We largely agree with this assessment: despite their clear systemic necessity, the business case for batteries is insufficient.

![]()

Figure 2. Economic viability by technology under high demand. Only large-scale batteries were evaluated.

The viability of BESS will grow primarily through additional revenue on the aFRR and mFRR markets through 2035, as higher capacity will be required in these markets. 70% of the revenue will come from the intraday market, while 30% will be generated from the equally growing day-ahead market. Grid tariffs will rise by 4.7% annually, but due to sharply declining CAPEX costs (the new-construction CAPEX for 2-hour, 4-hour, and 8-hour batteries is falling in real terms from 560, 1,000, and 1,780 €/kW in 2026 by approximately 55% toward 2035‘), the cost side for BESS will also decrease. This will result in a stronger business case starting in 2033.

A business case that is ‘likely viable’ for only slightly more than half of the projects starting in 2033 does not provide the stable investment climate needed to add nearly ten times the 2025 BESS capacity (1.5 GW) within 10 years. Furthermore, in all scenarios, TenneT assumes that 75 to as many as 100% of the BESS projects have a Time-Duration-Tied Transmission Right (TDTR) with the corresponding 50% discount on grid tariffs. The reality is that only a small portion of the projects have this type of contract, and the market is also unaware of any intention to offer TDTR to 100% of the BESS projects. Additional policy measures are clearly needed to actually reach 15.8 GW of BESS capacity by 2035.

Capacity mechanism to address shortages

TenneT rightly concludes that a capacity mechanism is needed to address future electricity shortages. Energy Storage NL previously wrote a position paper on the need for such a mechanism. TenneT sees a continued role for gas-fired power plants over the next ten years in ensuring security of supply, albeit to a decreasing extent. The government must be careful to ensure that the introduction of a capacity mechanism does not inadvertently provide further incentives for fossil-fuel power plants. The combination of a dispatch fee and an availability fee can be very attractive for existing assets that can supply low-cost power for extended periods (see also Figure 2, where the business case for gas-fired power plants compared to storage—without a mechanism—is already significantly better). In the long term, however, LDES will have to take over this task. Without a fair valuation of the contribution of storage, demand-side response, and interconnection—and a clear path toward carbon neutrality within the mechanism—there will be no business case for LDES, with fossil fuels lock-in as a result.

Call for Proposals by Energy Storage NL in Response to the Security of Supply Monitor

The 2026 Security of Supply Monitor shows that batteries will play an increasingly important role in the energy system and in ensuring security of supply. At the same time, the current and future business case for BESS is shaky. This uncertainty creates a poor investment climate. In addition, a poorly designed capacity mechanism poses the risk of fossil lock-in and current policy does not provide sufficient incentives for the sustainable alternative: LDES in the form of electricity, heat, and hydrogen storage.

Energy Storage NL is therefore asking grid operators to make the TDTR widely available as soon as possible, as seems to be suggested in the report. In addition, it is important to include LDES more explicitly in future plans and analyses. Long-term controllable capacity will remain essential in the future. It is important to ensure that this need is met by CO2-free technologies. The government needs to provide greater risk coverage for BESS and LDES, for example through targeted guarantees. Furthermore, revenue can be better guaranteed through flex tenders, an appropriate capacity mechanism, or a CfD. The costs of BESS can be better covered through discounts on grid tariffs. The report makes it clear that storage is no longer a peripheral condition, but a necessary pillar of supply security and the energy system. The next step is to translate that system value into a viable business case.

Latest News

Member News

Member News

Ore Energy Raises $43 Million to Unlock Renewable Base-Load Power for the AI Era

August 5, 2026 News

News

BlueTerra and Trinomics Study: Secondary Assets Offer Great Potential for Improved Congestion Management

July 31, 2026 News

News